- Microsoft is currently overvalued by about 20%. But is the market inclined to eliminate this overvaluation?

- Since the beginning of the year, the Nasdaq index has been growing along with gold, ignoring the dynamics of consumer spending.

- The main drivers of Microsoft’s recent capitalization growth are external and temporary.

- I will start with my standard introduction to clearly describe my paradigm of perception of what is happening in the stock market.

The stock market is best associated with a pendulum. It is in constant motion, but from time to time returns to a balanced (or rational) state. Therefore, if we are trying to predict the price of a company, we need to look for an answer to two questions. Firstly, what is the company’s current rational price. And secondly, what is the state of the market pendulum.

#1 What is Microsoft’s current rational price?

Very briefly. The following model best reflects the specifics of 2020 in the context of the rationality of Microsoft’s (MSFT) current price:

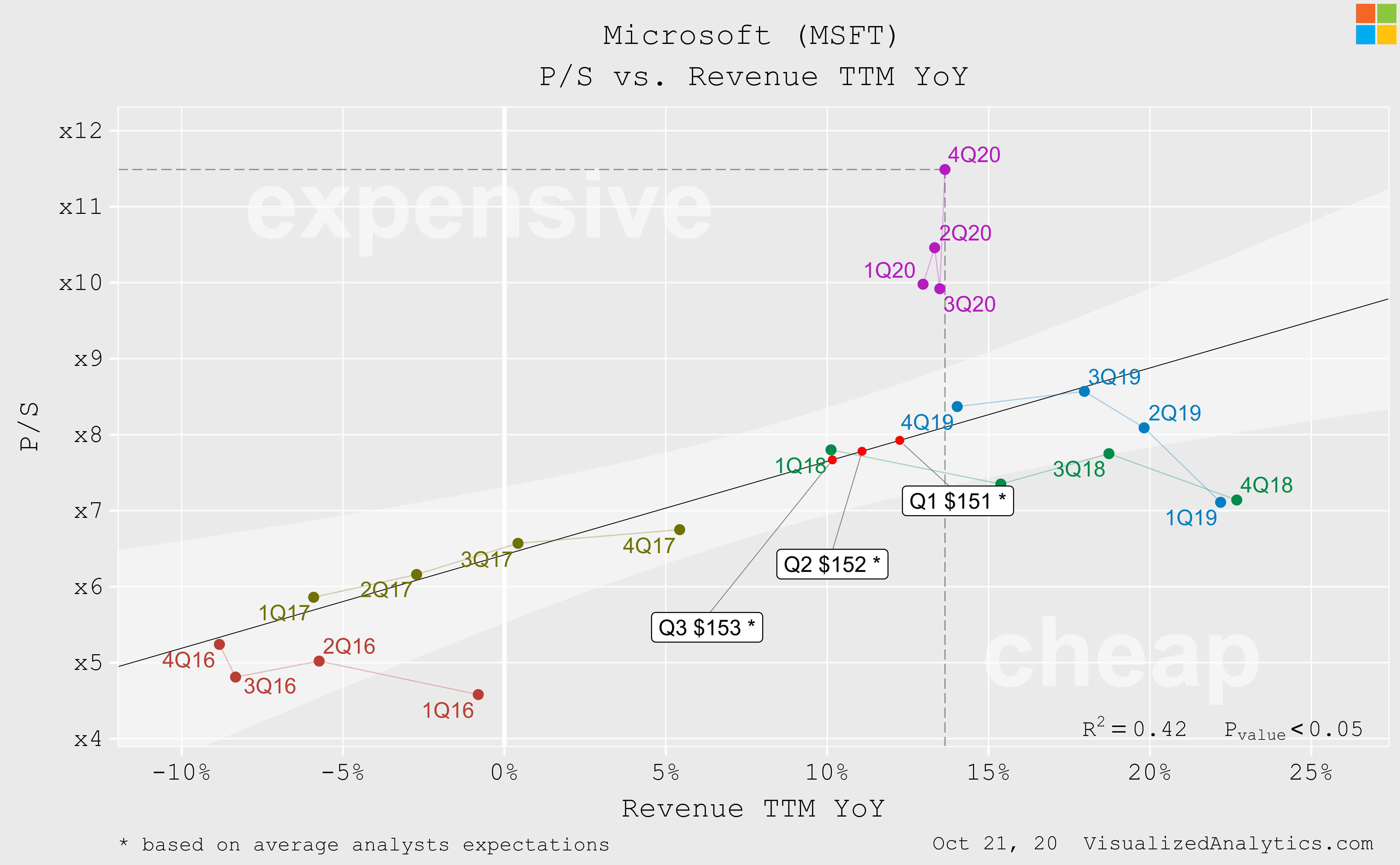

In the current year, Microsoft’s annual revenue growth rate showed no acceleration and forecasts are not encouraging either. But at the same time, the P/S multiple of the company showed a stable growth. Agree, other things being equal, this is not normal.

In the current year, Microsoft’s annual revenue growth rate showed no acceleration and forecasts are not encouraging either. But at the same time, the P/S multiple of the company showed a stable growth. Agree, other things being equal, this is not normal.

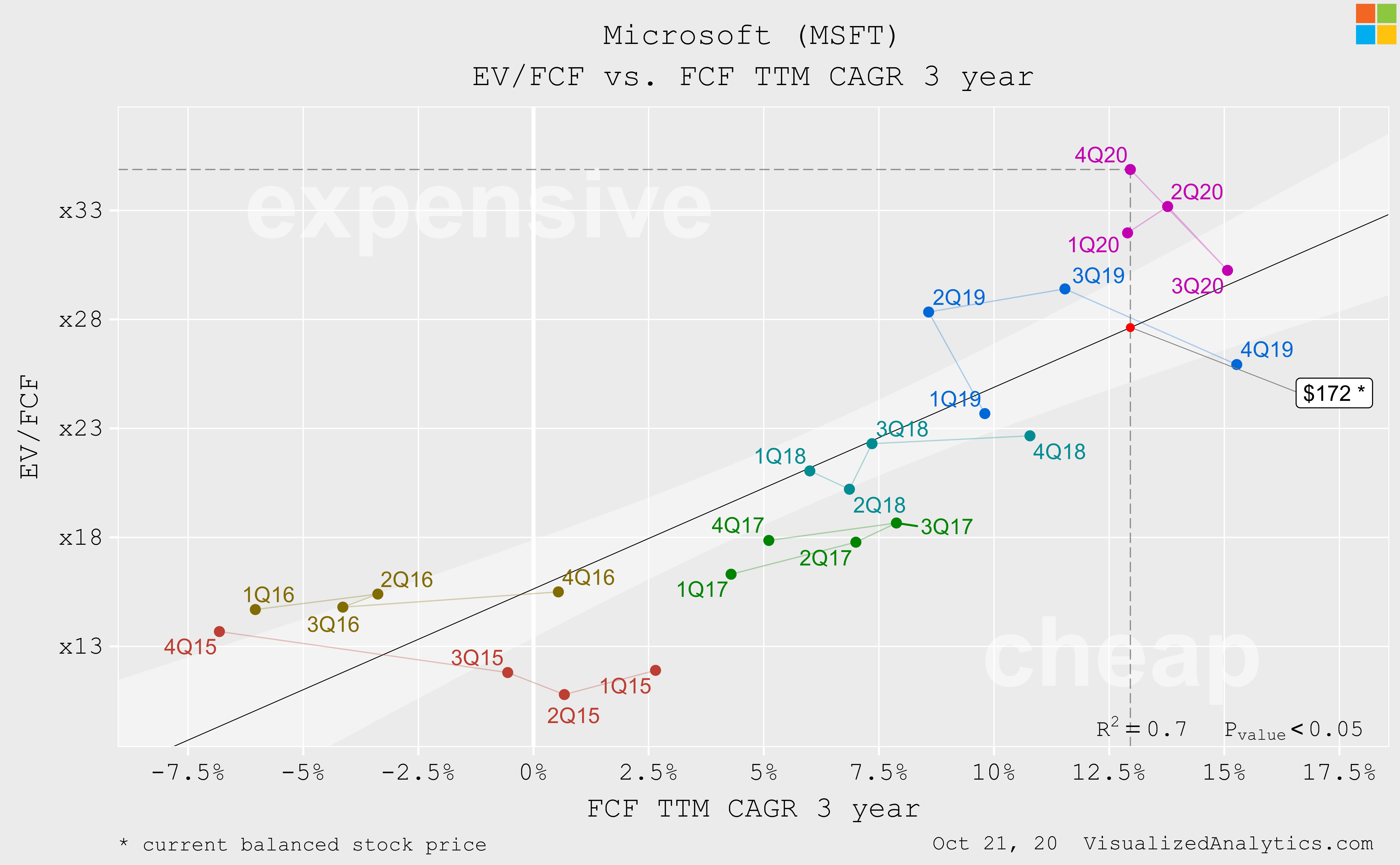

In the case of Microsoft, there is also a stable relationship between the growth rate of FCF and the EV/FCF multiple. And, judging by this relationship, MSFT’s market price is also overstated at the moment:

Now, let’s look at how the capitalization of Microsoft responds to the growth of its absolute financial indicators. There are also a number of qualitative dependencies, all of which characterize Microsoft as overvalued:

Now, let’s look at how the capitalization of Microsoft responds to the growth of its absolute financial indicators. There are also a number of qualitative dependencies, all of which characterize Microsoft as overvalued: